By Sebastian Carneiro, CEO & Co-Founder, with contribution from Christina Hounisen, Analyst.

Europe’s energy transition has, for the past decade, been largely a supply-side story. Wind farms, solar parks, and battery storage systems have attracted the bulk of institutional capital. But the economics of that asset class are shifting, and with them the opportunity set for investors.

Maintaining the Infrastructure Premium in an Evolving Asset Class

Shorter Power Purchase Agreement (PPA) durations, “Pay-as-Nominated” contract structures, and record negative power price events across European markets in 2025 are gradually altering the investment proposition of utility-scale renewables. As renewable penetration reached 50% of total EU electricity supply in 2024, rapid deployment without adequate storage has introduced price volatility largely absent under the old Feed-in-Tariff and long term PPA regime.

Independent power producers are evolving from passive “build-and-hold” operators into active energy platforms that increasingly resemble utilities — with trading rooms, merchant exposure, and active management requirements. As Gerard Reid noted on the Redefining Energy podcast earlier this year, private equity is stepping in to build the platforms suited to managing this new generation of assets and commanding higher returns accordingly.

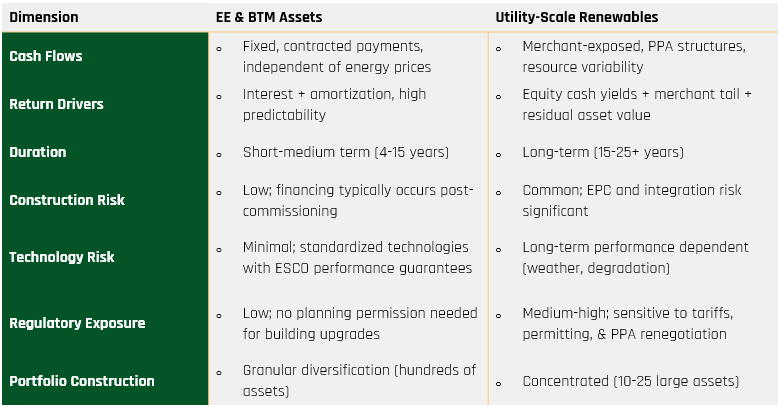

While utility-scale renewables remain central to Europe’s climate and energy independence targets, their increased exposure to volatile power prices alters their fit within infrastructure portfolios traditionally constructed around predictable, asset-backed cash flows. For institutional investors, Energy Efficiency (EE) and Behind-the-Meter (BTM) assets offer a strategic opportunity to maintain a resilient energy transition allocation that delivers regular pay-outs without electricity price risk.

The Structural Alternative: Energy Efficiency and Behind-the-Meter as a De-Risked Allocation

On the demand side of the energy system stands an underfunded asset class central to Europe’s climate and energy security targets. The decarbonisation of buildings and industrial facilities — through EE and BTM assets — represents the third pillar of the energy transition. EE and BTM assets sit behind the meter, insulated from wholesale electricity price risk and bypassing congested grids entirely, offering meaningful diversification within existing energy infrastructure portfolios.

The €150 Billion Investment Opportunity — and the Regulatory Drivers

Buildings account for 40% of EU energy consumption, and 75% of Europe’s building stock remains energy inefficient, with renovation rates at just 1% annually. This creates a €150+ billion annual investment gap through 2030. The 2022 energy crisis — which saw EU industrial electricity prices roughly double those in the United States — placed energy efficiency at the top of the pan-European political agenda. In direct response, RePowerEU set a target of 30 million heat pumps by 2030 alongside ambitious building renovation mandates.

Regulatory forces are now making the investment case structural:

- The European Performance of Buildings Directive – EPBD (2024): Binding minimum energy performance standards require the worst-performing 16% of non-residential buildings to be upgraded by 2030 and 26% by 2033, with residential buildings achieving a 16% reduction in primary energy use by 2030 and 20–22% by 2035 — setting a compliance clock for building owners across Europe.

- European Trading Scheme 2 – ETS2 (from January 2027): Carbon pricing extends to the buildings sector. With CO₂ prices projected at €45–55 per tonne by 2030, an EE Class G building will face €800–€1,200 higher annual costs than a Class B equivalent. Inefficient properties already face valuation discounts, whilst efficient buildings command sale price premiums of 3–15% in residential and 13–20% in commercial real estate — signals that will only intensify.

- EU Pillar 3 ESG Disclosure (in place): Banking regulation is explicitly targeting energy efficiency in buildings, making the energy performance of real estate assets and mortgage lending activities an active risk management and disclosure obligation. To qualify as EU-Taxonomy, the underlying property of mortgages must achieve Energy Performance Class A or fall within the top 15% most efficient of the national building stock.

The Financing Mechanism: Energy-as-a-Service

The core of the investment thesis rests on the Energy-as-a-Service (EaaS) financing model. Building owners face a well-documented barrier: the technologies are proven and the economics are attractive, but upfront capital stops most projects before they start. EaaS removes that barrier entirely. A specialised Energy Service Company (ESCO) finances, installs, and maintains all equipment — heat pumps, LED lighting, building management systems, rooftop solar — at zero upfront cost. The building owner signs a long-term service contract at a fixed fee set below current energy costs, with savings guaranteed from day one.

This creates a win-win-win structure: building owners achieve immediate cost reduction with no capital outlay; ESCOs secure long-term contracted revenue; and institutional investors providing the underlying project finance receive fixed, fully amortising cash flows backed by essential building services.

Solas Capital acts as the bridge: By understanding both the funding needs of project partners and requirements of investors, we are the financial intermediary, providing the necessary project funding for ESCOs to install integrated decarbonisation solutions across building facilities. In turn, investors get an infrastructure quality and EU-Taxonomy eligible allocation with fixed-income type returns.

What This Looks Like in a Portfolio Context

For institutional investors, EE and BTM investments offer a strategic opportunity to maintain a resilient energy transition allocation that deliver a de-risked strategy with fixed-income type returns due to three distinct characteristics:

- Cash Flow Predictability: 8–15-year service agreements with fixed, fully amortising offtake structures align naturally with pension fund and insurance company liability profiles, whilst the placement of assets behind the meter eliminates exposure to wholesale power price fluctuations.

- Seniority of Payment: Energy for heating, cooling, and industrial processes is non-discretionary — these are the last services cut by building occupants during economic downturns, which creates resilient cash flows.

- Asset-Backed Security with Proven Performance: Physical equipment — heat pumps, solar installations, building management systems — provides tangible collateral, with performance guaranteed by the ESCO — minimize technology risk.

For investors with sustainability mandates, these assets are EU Taxonomy-eligible and classify under SFDR Article 9, delivering measurable, verified emissions reductions alongside infrastructure-quality returns.

The Investor Implications

For the institutional investor, the takeaway is clear: the next phase of the energy transition will be won at the point of consumption, and accessing this opportunity through specialized partners like Solas Capital enables diversified exposure to building decarbonisation whilst preserving traditional infrastructure allocation characteristics. Investing with an ‘energy system as a whole’-approach is now a strategic imperative for maintaining resilient energy infrastructure portfolios aligned with Europe’s security, competitiveness, and climate objectives.

About the Authors:

Sebastian Carneiro: Sebastian is the Chief Executive Officer & Co-founder of Solas Capital AG, a specialised investment advisory firm that finances solutions for decentralised energy efficiency and behind-the-meter assets across Europe. Sebastian has over 15 years of experience in project finance, including his previous role as Director at Europe’s largest private energy efficiency fund. As a CFA Charterholder and engineer by trade, Sebastian is driven by dev-eloping innovative investment solutions that accelerate the deployment of green assets and make the energy transition a reality.

Christina Hounisen: Christina is a Business Development & Operations Analyst at Solas Capital. Her background spans energy policy at the IEA, private sector renewable energy from a leading global offshore developer, and sustainability consulting. She holds a MS in Sustainability & Social Innovation from HEC Paris and a BSc in International Business & Politics from Copenhagen Business School.

For any questions, please contact info@solas.capital